Remote Appointment Setters Learn How to Buy a Small Business for Entrepreneurial Success

Introduction — Why this guide matters for remote appointment setters

Are you a remote appointment setter in 2026, working hard but feeling like you don’t have full control? Maybe you’re tired of relying only on commissions, hoping for that next big sale to pay the bills. It’s a common feeling. While finding remote work is great, and learning how to make money online as a remote appointment setter can be very rewarding, many folks dream of something more stable and their very own.

Here’s a big idea: What if you could buy a small business? For many, this sounds like a huge step, but it can actually be a smart way to get a steady income and be your own boss. Imagine using your great communication skills, the ones you’ve perfected by finding leads and setting meetings, to run your own company. Becoming a business owner gives you more say over your time, your money, and your future.

Of course, it’s normal to have worries. You might think, "I don’t know anything about buying a business!" or "What if I get scammed?" These are real concerns. It’s true that online marketplaces need to do a good job checking who sellers are to build trust for everyone involved, including buyers like you [1]. In fact, laws like the INFORM Consumers Act even require marketplaces to get information from high-volume sellers [2]. This helps make things safer. Plus, having a licensed business broker can help protect your deal [3].

But don’t let those fears stop you. This guide is your easy-to-follow small business planner. We’ll walk you through the steps to help you find and buy a small business that’s a good fit for you.

We’ll show you how to look for legitimate chances, how to get money for your purchase, and how to use the skills you already have. This isn’t just about finding another job. It’s about taking charge and finding a clear path to become a successful business owner.

1) Why Buy a Small Business? Pros, Risks, and Fit for Remote Appointment Setters

You’re a remote appointment setter right now. You’ve learned how to talk to people, find what they need, and set up important meetings. These are super strong skills, and they can help you become a successful business owner. But why should you think about buying a small business instead of starting one from nothing? Let’s look at the good parts, the tricky parts, and what kind of business fits you best.

Buying vs. Starting: A Clearer Path to Being Your Own Boss

Imagine you want to open a small coffee shop.

- Starting from scratch means you have to find a place, buy all the machines, get permits, hire staff, and then hope people show up. It takes a lot of time and money before you even make your first cup of coffee. It can be exciting, but it’s also a big risk.

- Buying an existing business is different. It’s like buying a coffee shop that’s already open and making coffee. It already has customers, equipment, and maybe even staff. This means you can start earning money much faster. It’s often less risky because the business has already proven it can make money [1]. For many, this is a smarter way to become a business owner.

Your skills as an appointment setter are a great fit here. You know how to bring in new customers and keep them happy. That’s exactly what a good business owner needs to do! If you want to dive deeper into how your existing skills can help you make money online, you might find our guide on how to make money online in 2026 as a remote appointment setter useful.

What Are the Risks When You Buy a Small Business?

Even though buying a business can be safer than starting one, there are still things to watch out for.

- Money Risks: You’ll need money to buy the business. This could be from loans or your own savings [2]. Sometimes a business might have hidden problems that cost money to fix later.

- Running the Business: The business might have old ways of doing things that don’t work anymore. You might also have to deal with employees or systems that are new to you. Learning how to manage everything can be a big job.

- Good Name (Reputation): If the business you buy has a bad reputation or unhappy customers, it will be up to you to fix it. This can take a lot of work.

For remote owners, these risks can feel even bigger. You won’t be in the office every day to see what’s happening. You’ll need good ways to keep up with your team and customers from afar [3].

Great Small Business Ideas for Remote Appointment Setters

The good news is that many small business ideas are perfect for people who work remotely, just like you. In 2026, many businesses are online and use tools like AI to help them grow [4].

Here are some types of businesses that match your skills well:

- Client-Based Services: Think about businesses that offer services online, such as digital marketing agencies, virtual assistant companies, or online coaching. Your communication skills are key to getting and keeping clients. There are many innovative remote business opportunities available today [5].

- Lead Generation Models: You already know how to find leads. You could buy a business that specializes in finding new customers for other companies. This directly uses your main skill!

- Brokered Revenue Streams: This includes things like affiliate marketing or online marketplaces. You act as a link between buyers and sellers, much like you do when setting appointments. Affiliate marketing is still a strong online business model in 2026 [6].

- E-commerce: Buying an existing online store means you already have products and customers. You can use your sales skills to grow the business even more. E-commerce is a top trend for small businesses this year [7].

Remember, the goal is to find a business where your talent for talking to people and making connections can really shine. This way, you can build on what you already know and be a successful business owner.

2) Where to Find Legitimate Small Businesses for Sale (Marketplaces, Brokers, and Auctions)

So, you’re ready to find a small business that fits your remote appointment setter skills. That’s great! But where do you actually look to buy a small business? It’s important to know the right places so you can find a good, honest deal. Think of it like finding a treasure map to your next adventure.

The Best Places to Look for a Small Business

There are a few main ways to find businesses that are ready for a new owner in 2026.

- Online Marketplaces: These are websites made just for selling businesses. They’re like big online stores, but for entire companies.

- What to look for: On these sites, you’ll find many small business ideas. It’s smart to pick platforms that make sure the people selling are real. Some marketplaces use special checks to make sure sellers are who they say they are, which helps build trust for buyers like you [1]. The law even requires online marketplaces to get information from bigger sellers to keep things fair [2].

- Business Brokers: These are people who help buy and sell businesses. They’re like real estate agents, but for companies instead of houses.

- What to look for: When you work with a broker, make sure they are licensed and have special training. Good brokers have important papers like a Certified Business Intermediary (CBI) to show they know what they’re doing [3]. Using a credentialed broker can help protect you during the sale [4].

- Industry-Specific Listings: Sometimes, you can find businesses for sale on websites that focus on a certain type of industry. For example, if you want to buy a marketing agency, you might look at marketing industry websites.

- Public Auctions: This is less common for small businesses, but sometimes businesses are sold at auction. This might happen if a business needs to be sold quickly.

How to Check if a Listing or Broker is Good

Before you get too excited about a business, it’s super important to do your homework. This is called "vetting."

For Business Listings:

- Ask for Papers: The seller should be able to show you how much money the business has made (its finances) and how it runs. If they don’t want to share this, that’s a red flag.

- Check Their Story: Does what they say about the business make sense? For example, if it’s an online store, does it actually have products and a real customer base?

- Look for Verification: Good online marketplaces often have ways to check if businesses are legitimate [5].

For Business Brokers:

- Ask About Credentials: Remember those special papers like CBI? Ask to see them. This shows they are experts [3].

- Check Their Reputation: What do other people say about them? Do they have a good name?

- Understand Their Role: A good broker helps both the buyer and the seller, making sure everything goes smoothly.

Picking the Right Business for You

As a remote appointment setter, you know how to find the right fit for clients. Use those same skills here! When you look at different listings, think about:

- How Much Money It Makes: Does the business bring in enough money for you to live comfortably? You want a business that’s already doing well.

- How Much You Need to Do: As a remote business owner, you might not want a business that needs you to be there all the time. Look for one where you can manage things from afar.

- Fits Your Skills: Does it match your ability to talk to people and set appointments? If you’re skilled at outreach and client relations, a service-based business or a lead generation model might be perfect. Our guide on how to become a remote appointment setter in 2026 can help you remember all the skills you bring to the table.

- Location Flexibility: Can this business truly be run remotely, or does it need you to be in a specific place?

Choosing the right small business planner means finding a good match for your skills and how you want to work. Take your time, ask lots of questions, and don’t be afraid to dig deep into the details.

You’ve found a great small business idea that you want to buy. That’s a huge step! Now comes the next big question: How will you pay for it? Knowing your money options is key to becoming a successful business owner.

Ways to Pay for Your Small Business

There are several common ways to finance your purchase in 2026. Each one works best for different situations.

- SBA Loans (Small Business Administration Loans): These are very popular for people who want to buy a small business. The government helps banks offer these loans, making it easier for buyers to get money.

* **What they are:** SBA loans, especially the 7(a) program, help small businesses by guaranteeing a part of the loan to the lender. This means banks take less risk, so they are more likely to lend money to you <sup>[7]</sup>. These loans can be used for many things, like buying a business, getting equipment, or refinancing old debt <sup>[6]</sup>.

* **What to expect:** You can get up to $5 million with an SBA 7(a) loan for business purchases <sup>[4]</sup>. Many banks, credit unions, and online lenders offer them <sup>[2]</sup>. In 2026, there are many choices for these loans <sup>[1]</sup>. For more details on these, you might find this [2026 Guide to SBA Loans & Digital Acquisitions](https://www.youtube.com/watch?v=sNd3cEBO2OE) helpful.

- Bank Loans: You can also go to a regular bank or credit union to get a business acquisition loan. These are often called "term loans."

- What they are: Banks provide the money directly. They will look closely at the business’s past money-making and your own financial health.

- What to expect: Banks want to see that the business is strong and that you have a good plan for running it. Loans can range from $25,000 up to $500,000 from some banks [6].

- Seller Financing: Sometimes, the person selling the business will also help you pay for it.

- What it is: The seller agrees to let you pay them back over time, often with interest. This is like getting a loan directly from the seller.

- When it makes sense: This is great for smaller businesses or when a seller really believes in the business and wants the new owner to succeed. It can also show other lenders that the seller has faith in the business’s future.

- Creative Structures (Like Earn-outs): These are less common but can be very helpful.

- What they are: With an "earn-out," you pay part of the price now and then more later, based on how well the business does after you buy it.

- When it makes sense: This is good for businesses where the future growth is a bit uncertain or if the seller wants to stay involved for a short time to help you grow it.

- Personal Funds: You can also use your own savings or money from family and friends to buy a small business.

When Each Option Is Best

- SBA and Bank Loans: These are often best for bigger deals where the business has a clear history of making good money. Lenders will check your credit history and how much money the business makes each month (cash flow) to make sure you can pay back the loan [3].

- Seller Financing: This option works well for smaller businesses or when you don’t quite meet all the strict rules for a bank loan. It also shows that the seller is confident in the business and its future with you as the new business owner.

- Earn-outs: These are useful if the business has a lot of potential for growth that hasn’t happened yet, and the seller wants a share of that future success.

Getting Ready to Ask for Money

To get approved for a loan or financing, you need to show that you’re prepared. Think of yourself as a small business planner, even before you buy the business.

- Show Your Numbers: Gather all the business’s money papers. This includes tax returns, profit and loss statements, and balance sheets. Lenders want to see that the business is healthy and makes enough money to cover loan payments [1].

- Write a Business Plan: This is like a roadmap for how you will run the business. It shows what the business does, who its customers are, and how you will make it grow. A clear plan helps lenders trust your vision.

- Create a Forecast: This is your best guess about how much money the business will make in the future. It should be realistic and show how you plan to increase sales and profits. Your understanding of small business policy can also make you a stronger business owner and a more attractive borrower.

Knowing these steps will make it much easier to buy small business and start your journey as a business owner.

Valuation & Due Diligence: How to Assess a Small Business Before You Buy

Once you know how you’ll pay for a small business, the next big step is figuring out how much it’s really worth. You also need to check everything about the business to make sure there are no hidden problems. This process is called valuation and due diligence. It helps you become a smart business owner.

How to Figure Out a Business’s Worth

When you want to buy small business, you need to know its fair price. There are a few common ways to value a business in 2026:

- Income Approach: This method looks at how much money the business makes or is expected to make in the future. It’s often used for small businesses because it focuses on the cash flow you’d get as the new owner [3]. One common way here is "earnings multiples," which means you multiply the business’s yearly earnings by a certain number [2].

- Market Approach: This is like looking at how much similar houses sold for in your neighborhood. You compare the business you want to buy to other businesses that have been sold recently [2]. This helps you see what’s a normal price for that type of small business idea.

- Asset Approach: This method adds up the value of everything the business owns, like its buildings, equipment, and inventory, and then subtracts any debts [3]. This approach is usually better for businesses that own a lot of physical things, like manufacturing companies, rather than service businesses.

Many experts use a mix of these methods to get the best idea of a business’s true worth [6].

Checking Everything: Your Due Diligence Checklist

Before you hand over any money, you need to dig deep into the business’s details. This is your chance to play detective and make sure the business is as good as it seems.

- Money Matters: Ask for all financial records, like tax returns for the last few years, profit and loss statements, and bank statements [1]. You need to see if the business truly makes money and how steady its earnings are.

- Legal Stuff: Check for any lawsuits, important contracts with customers or suppliers, and necessary permits or licenses. You want to make sure the business is following all the rules and doesn’t have big legal problems hanging over it.

- Customers and Sales: Who are the main customers? Are they loyal? How does the business get new customers? Understanding this helps you see if the business has a strong base to grow from.

- How it Works: Look at the day-to-day operations. How are products made or services delivered? Who are the key employees, and what makes them stay? A smooth operation means fewer headaches for you.

- Contracts: Get copies of all major agreements, such as leases for buildings, contracts with big suppliers, or employment agreements for important staff. These show ongoing costs and responsibilities.

Getting Help from Experts

You don’t have to do all this checking alone. Actually, it’s really smart to get help from people who do this for a living.

- Accountants: A good accountant can go through all the financial papers to make sure they are correct and that the business is truly profitable. They can spot hidden costs or money problems.

- Lawyers: A business lawyer can review all the legal documents and contracts. They’ll make sure you understand what you’re agreeing to and protect you from legal risks.

These advisors can help you request the right documents early on. They can also help you spot any "deal breakers," which are problems so big you might decide not to buy the business at all. Understanding things like small business policy also makes you a better business owner, helping you know what questions to ask and what to look for when assessing a business.

By carefully valuing the business and doing thorough due diligence, you’re setting yourself up for success when you decide to buy small business and become a new business owner.

5) Negotiation and Deal Structure: Protecting Yourself in the Purchase Agreement

After you’ve looked closely at a business and figured out what it’s worth, the next big step is to talk about the price and write down the rules of the sale. This part is called negotiation and deal structure. It’s where you make sure you’re protected when you buy small business. Think of it like making a really important plan and putting it in writing.

Key Things to Talk About in Your Contract

When you’re ready to buy a small business, the purchase agreement is your most important document. It needs to clearly say what both you and the seller are agreeing to. Here are some key points to negotiate:

- Price Adjustments: Sometimes, the final price might change a little. This can happen if things look different right before you close the deal than they did when you first agreed. For example, if the business has less inventory than expected.

- Representations and Warranties: These are like promises from the seller. They say certain things about the business are true and accurate. For instance, the seller might promise that all financial records are correct or that there are no hidden lawsuits. If these promises turn out to be false, you have a way to get some money back or even cancel the deal.

- Escrow: This is when a part of the money you pay is held by a neutral third party for a short time after the sale. It’s like a safety net. If problems come up later, like an unexpected bill from before you owned the business, the money in escrow can be used to fix it.

- Covenants Not to Compete: This is really important. It’s an agreement where the old business owner promises not to open a similar business nearby or try to steal your customers for a certain time. This helps you keep the customers you just bought.

Making the Deal Work: Bridging Price Gaps

Sometimes, you and the seller might not agree on the exact value of the business. You might think it’s worth a bit less, and they might think it’s worth more. That’s okay! There are ways to make the deal fair for everyone:

- Earn-outs: With an "earn-out," you pay part of the price upfront, and then the seller gets more money later if the business does well under your ownership. It’s a way for the seller to earn extra if your small business ideas prove successful.

- Performance-Based Clauses: These are similar to earn-outs. They mean some payments are tied to how the business performs in the future. If sales hit certain goals, the seller gets an extra payment. This can help both sides feel good about the deal.

How Buyer Protections Work

Whether you’re an individual buying your first small business or a big company, you need protections in the deal. For someone like you, a new business owner, these protections often come from clear, simple language in the contract that covers the points above. You’ll rely on your lawyer to make sure these terms are strong. Big companies might have lots of lawyers and complex strategies, but the goal is the same: to make sure you get what you pay for and are safe from unexpected problems. Understanding how small business policy affects these agreements can really help you as a smart business owner.

Make sure you work closely with your lawyer and accountant during this negotiation phase. They are your best guides to make sure the purchase agreement protects you fully.

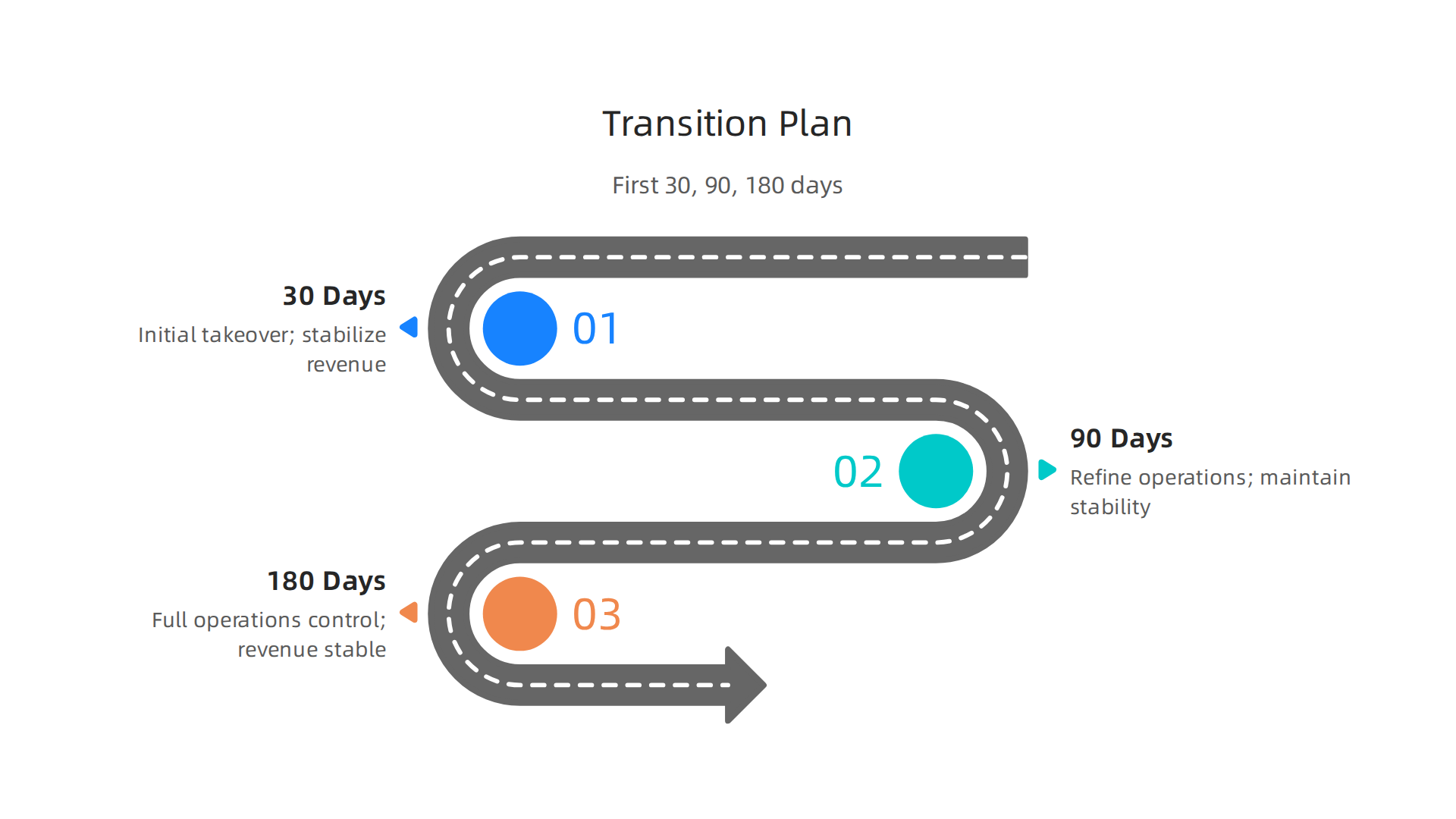

6) Transition Planning: Taking Over Operations and Keeping Revenue Stable

After you’ve agreed on the price and signed all the papers to buy a small business, the real work of making it your own begins. This next step is called transition planning. It’s all about moving smoothly into your new role as a business owner, making sure nothing breaks, and that money keeps coming in. Think of it like taking the steering wheel of a car that’s already moving. You want to make sure you drive it well without any sudden stops.

A smart business owner will have a plan for the first few months, often broken into 30, 90, and 180-day steps.

This helps you know what to focus on and when, making sure your small business ideas start strong.

Your First 30, 90, and 180 Days

This special plan helps you take over without missing a beat. Many experts suggest using checklists to guide you through this time, covering everything from people to money to technology [source: Burnie Group, Lutz].

-

First 30 Days: Settle In and Listen

- Talk to Customers: Reach out to your best customers. Let them know you’re the new owner and that you’re excited to keep serving them well. Ask them what they love about the business.

- Meet Your Team: Get to know your staff. Learn their names, what they do, and what they worry about. Keeping good staff happy is key to keeping the business running smoothly [source: The Predictive Index].

- Learn the Ropes: Watch how everything works. How are products made? How are services given? What tools do people use every day? This is like mapping out the business’s heart.

-

Next 60 Days (Days 31-90): Make Small, Smart Changes

- Check Systems: Now that you know how things work, look for small ways to make them better. Maybe a new way to track customer calls or order supplies.

- Train Staff: If you see a need for new skills, start offering training. This could be anything from using a new computer program to learning how to talk to customers even better.

- Keep Talking: Continue to communicate with your customers and staff. Keep them updated on any changes and make sure they feel heard. Having an integration roadmap helps here [source: Website Closers].

-

Beyond 90 Days (Days 91-180): Plan for Growth

- Big Ideas: With a good handle on things, you can start putting your bigger small business ideas into action. This might mean adding new services or finding new customers.

- Check on Goals: Look back at your plan. Are you hitting your goals for keeping customers and making money? Adjust if needed.

Keeping New Customers Coming In

During this busy time, you need to make sure new customers keep finding your business. This is where people called remote appointment setters can be a big help. They can make calls or send messages to potential customers, setting up meetings for you or your sales team. This helps preserve your lead flow, meaning you always have new opportunities. You might even consider learning more about how to make money online in 2026 as a remote appointment setter or exploring how to become a remote appointment setter to understand their work better. They can also help you train your existing staff on new ways to talk to customers and manage communications.

Key Things to Check Off Your List

To make sure your new business is on solid ground, you’ll need a checklist for operations. Experts often use detailed checklists for merging businesses that cover many areas [source: MergerIntegration.com]. Here are some important items:

- Customer Records (CRM): Make sure you take full ownership of all customer information. This includes lists of past customers and details of how they like to be served.

- Vendor Contracts: Review agreements with companies that supply your business with goods or services. Make sure they are still good and fair.

- Payroll: Understand how employees are paid and make sure everything is set up correctly for you to take over.

- Legal Steps: Check that all legal paperwork, like business licenses and permits, are transferred to you and that you are following all the rules [source: ACC].

By planning carefully and taking these steps, you can successfully buy small business and guide it into a bright future.

7) Buying as a Career Move: How Remote Appointment Setters Can Leverage Business Ownership

If you’re already a remote appointment setter, you know a lot about talking to people, finding new customers, and solving problems. These skills are actually perfect if you want to buy a small business.

Think of it: you’ve been helping other businesses grow; now you can use those talents to grow your very own.

Your Appointment Setting Skills are a Secret Weapon

Many of the things you do as a remote appointment setter are exactly what a successful business owner needs to do every day.

- Finding Customers (Lead Generation): As an appointment setter, you’re a pro at finding people who might be interested in a product or service. This skill is gold for any small business owner who needs to keep new customers coming in. In 2026, finding good leads is still a top priority for businesses, often using new sales strategies [source: CO].

- Talking to People (Objection Handling): You know how to listen and help people understand why something is a good fit. When you own a business, you’ll use this skill to talk to customers, deal with any issues, and even explain things to your staff.

- Staying Organized (CRM Usage): You likely use tools to keep track of customer talks and appointments. This helps you manage many conversations at once. When you buy a small business, you’ll need similar systems, called CRM (Customer Relationship Management) tools, to keep all your customer information neat and ready. Many small businesses are using smart AI tools to help with sales and customer service in 2026 [source: Centre Daily Times].

- Knowing What Customers Want: You’re always trying to figure out what customers need so you can set up the best appointments. As a business owner, this helps you offer the right products or services.

When to Buy Versus Stay an Employee

Deciding to buy small business is a big step. It’s about wanting more control and a bigger reward for your hard work. As an employee or contractor, your earnings might be capped. But as a business owner, you have the chance to grow the business and, in turn, grow your own wealth. Buying an existing business means you skip many of the hard parts of starting from scratch. You already have customers, staff, and a product. This can be a great way to take your career to the next level in 2026, especially with many new online business ideas becoming popular [source: Network Solutions].

Paths to Grow or Sell Your Business

Once you’ve bought a business, your journey doesn’t stop. You can make it bigger in many ways. You might add new services, reach new types of customers, or even open new locations. Some owners look into franchising their successful business idea. And if you decide later that it’s time for a new adventure, you can always sell the business. That’s right, you can sell a business just like you bought one, allowing you to get back the money you put in and more.

Building these skills as an appointment setter can be your first step toward becoming a successful business owner.

Want to learn more about developing these valuable skills? Discover how to become a remote appointment setter in 2026 and set yourself up for future business success.

Learn How to Become a Remote Appointment Setter

Summary

This guide explains how remote appointment setters can move from commission work to owning a small business by buying an existing company. It walks through why buying often beats starting from scratch, which business types match appointment-setting skills, and where to find legitimate listings and credentialed brokers. The article covers financing options (SBA loans, bank loans, seller financing, earn-outs), basic valuation approaches, and a practical due diligence checklist of financial, legal, customer, and operational items. It also explains negotiation points to protect buyers—price adjustments, representations, escrow, and non-competes—and suggests deal structures to bridge price gaps. Finally, it gives a 30/90/180-day transition roadmap to keep revenue stable and shows how appointment-setting skills translate into customer acquisition and growth. After reading, you’ll know where to look, how to evaluate and finance a purchase, how to protect yourself in the contract, and how to run the business remotely once you take over.